Home Loan Eligibility at Salary 50K: How Much Home Loan Can You Get on ₹50,000 Salary?

Many people dream of owning a home, but most feel unsure about loan eligibility. This article explains home loan eligibility at salary 50k for a reference, it will help set realistic expectations and prevents financial stress later.

The article also shows how a home loan eligibility calculator supports better planning. And by the end, readers will know what loan amount to expect, what factors influence approval, and how to improve eligibility.

How Banks Calculate Home Loan Eligibility

Banks follow a structured method to calculate eligibility. They focus on income stability, repayment capacity, and financial discipline. While policies vary slightly, the core logic remains consistent.

Key Factors Banks Consider

Net monthly income

Existing EMIs or liabilities

Age and working years

Job stability and employer type

Credit score

Loan tenure

Applicable interest rate

Among these, income and EMI affordability play the most important role.

EMI Rule That Drives Eligibility

Banks allow only a portion of income for loan repayment. This rule protects borrowers from over-commitment.

Most lenders allow 40%–50% of monthly income as total EMI.

Example

Monthly salary: ₹50,000

Safe EMI range: ₹20,000 to ₹25,000

Banks use this EMI limit to calculate the maximum loan amount.

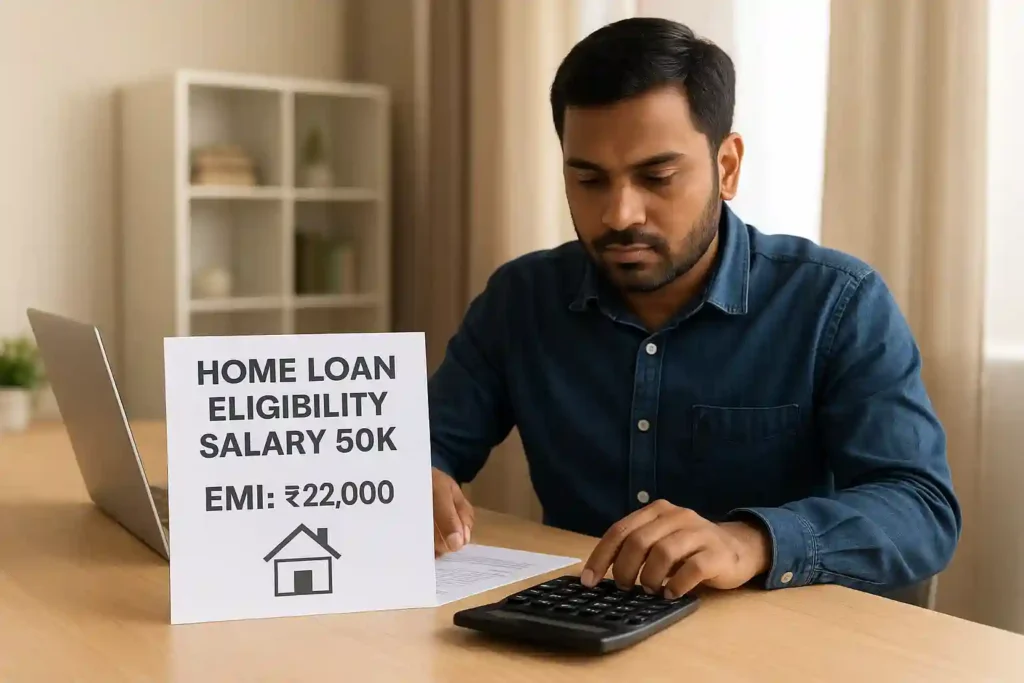

Home Loan Eligibility at Salary 50K: Expected Loan Amount

Let us convert EMI capacity into loan value using common assumptions.

Assumptions

EMI: ₹22,000

Interest rate: 9% per annum

Loan tenure: 20 years

Estimated Eligibility

₹26 lakh to ₹30 lakh

Most salaried applicants with a stable job fall within this range.

You can check Home Loan Eligibility Calculator here

Why a Home Loan Eligibility Calculator Matters?

A home loan eligibility calculator provides instant and personalized estimates. It uses income, tenure, and interest rate to calculate eligibility accurately.

Benefits of Using a Calculator

Shows loan amount instantly

Helps plan EMI comfortably

Avoids unrealistic property selection

Reduces rejection risk

You can check eligibility tools here:

Impact of Loan Tenure on Eligibility

Loan tenure directly affects EMI and loan amount. Longer tenure reduces EMI and increases eligibility.

Tenure Comparison

15 years: Higher EMI, lower loan

20 years: Balanced EMI and interest

30 years: Lower EMI, higher total interest

For a ₹50,000 salary, 20–25 years works best for most borrowers.

Credit Score and Its Role in Approval

Credit score strongly influences both approval and interest rate.

CIBIL Score Impact

750 and above: Best rates and fast approval

650–749: Approval possible with conditions

Below 650: High rejection risk

Regular and timely repayments help maintain a healthy score.

Effect of Existing EMIs

Existing loans reduce eligibility because banks deduct those obligations from income.

Example

Salary: ₹50,000

Existing EMI: ₹5,000

Reduced available EMI: ₹17,000–₹20,000

This reduction can lower eligibility by several lakhs.

Joint Home Loan: A Smart Strategy

Adding a co-applicant increases eligibility by combining incomes.

Who Can Join as Co-Applicant

Spouse

Earning parent

Earning sibling (in some cases)

Advantages

Higher loan amount

Better approval chances

Improved affordability

Many first-time buyers use this option successfully.

Down Payment Requirement

Banks usually finance 75%–90% of property value.

Illustration

Property price: ₹40 lakh

Loan approved: ₹30 lakh

Down payment: ₹10 lakh + charges

Planning down payment early makes the buying process smoother.

Step-by-Step Guide to Improve Eligibility

Close or reduce existing EMIs

Improve your credit score before applying

Choose a longer tenure carefully

- Negotiate interest rateswith lenders

Add a co-applicant

Avoid job changes during application

Declare all stable income sources

These steps improve approval chances without increasing salary.

Regulatory Framework

Banks follow RBI and National Housing Bank guidelines to ensure responsible lending.

👉 Visit the Reserve Bank of India official website to explore on guidlines

Conclusion: Can You Get a Home Loan on ₹50,000 Salary?

Yes, a ₹50,000 monthly salary allows you to qualify for a home loan under standard banking norms. In most cases, home loan eligibility at salary 50k falls between ₹25 lakh and ₹30 lakh, assuming a stable job and clean credit profile.

A home loan eligibility calculator helps set realistic expectations and improves planning. With disciplined finances and smart decisions, home ownership becomes achievable even at this income level.

Recent Posts

FAQ (Frequently Asked Questions)

Most borrowers can get ₹25–35 lakh, depending on EMI capacity, tenure, and interest rate.

Ideally, EMI should stay within ₹20,000–₹25,000.

Yes. A higher score increases eligibility and lowers interest rates.

Yes, but eligibility reduces based on current obligations.

A 25–30 year tenure balances EMI comfort and eligibility.

Yes. Adding a co-applicant can significantly raise loan amount.

Often yes, due to income stability and lower risk.

Calculators give close estimates but final approval depends on lender assessment.

Yes, with consistent income proof and strong credit history.

Yes, especially under affordable housing segments with proper planning.